How Nigeria’s $428 million ICT project is addressing rural financial inclusion

Until last year, Maureen Pam, a trader, always had to endure trekking to Ganawuri, a district in Plateau’s Riyom area, at the close of Friday market day at Vwang Market in Vom, Jos South.

She was always fear-stricken, caused by her previous experiences with armed robbers on the route, who stole the money she made from her sales that day.

Due to the unavailability of banks in these rural communities, most traders like Ms Pam had to return with the cash from sold goods to their homes, pending when they could access the closest bank, which is located over 60 kilometres from Ganawuri.

“On other weekdays, my daughter would take the money to the bank, but on Fridays, we often had to return with the money since most banks [in Jos-Bukuru metropolis] close early,” she said.

However, she now deposits her money into her bank account via agency bankers (commonly known as POS).

Agency banking allows customers to deposit and withdraw money instead of going to the bank or using ATMs. Currently, there is one agency banking agent for every 80 Nigerians and one bank branch for every 27,000, according to a 2023 report on the Nigerian Financial Services Market.

Although rural communities like Vwang and Ganawuri comprise 53 per cent of Nigeria, the World Bank in 2008 said only 2 per cent of rural households in the country were financially included.

The way out: A National ICT Backbone Project

In a bid to bridge the connectivity gap across the country, the Nigerian government, through its public enterprise Galaxy Backbone Limited signed a commercial contract worth $117 million with Huawei Technologies to commence the first phase of the Nigeria National Information and Communication Technology Infrastructure Backbone (NICTIB) Project.

This phase, completed in August 2018, covered 13 states, including Abuja, Benue, Nassarawa and other states in Southern Nigeria.

According to research by AidData, under the terms of the PBC agreement, the Government of Nigeria was responsible for paying 15 per cent of the cost of the commercial contract with Huawei Technologies Co. Ltd prior to project implementation.

However, Nigeria’s contribution was delayed until December 2006 when Galaxy Backbone Limited made an advance payment of $10 million to Huawei Technologies Co. Ltd. Later, in December 2013, the Federal Ministry of Finance of Nigeria — on behalf of Galaxy Backbone Ltd — completed the payment ($7.65 million) to Huawei to mark the official commencement of the project.

Two years after the completion of the first phase, Galaxy Backbone Limited commenced the second phase worth $328 million—funded via an Export Buyer’s Credit by the Export-Import Bank of China; this phase covers 19 states within Northern Nigeria including Plateau, Kaduna, Bauchi and Gombe, it was also contracted to Huawei Technologies.

In March 2020, Nigeria’s Debt Management Office (DMO) reported that the China Eximbank had disbursed 100 per cent of the original face value of this loan; the final maturity date of this loan being 21 September 2032, after a seven-year grace period.

Meanwhile, as of December 2022, phase two of NICTIB was 98 per cent completed. “At the completion of the project, it will deepen broadband penetration in Nigeria, which is targeted to reach 70% by 2025, up from its current 44.5%,” says Muhammad Abubakar, Managing Director of Galaxy Backbone Limited.

At the time of filing this report, Galaxy Backbone Limited had yet to respond to comments regarding the project’s current status.

According to Retna Daser, a telecom analyst and E.M Application Technologies, the NICTIB has made it easier for telecommunication companies like MTN, GLO and Airtel to rent a portion of the fibre to expand their connectivity into rural communities. “That’s the thing about fibre; multiple companies can route their data through an existing one,” he said.

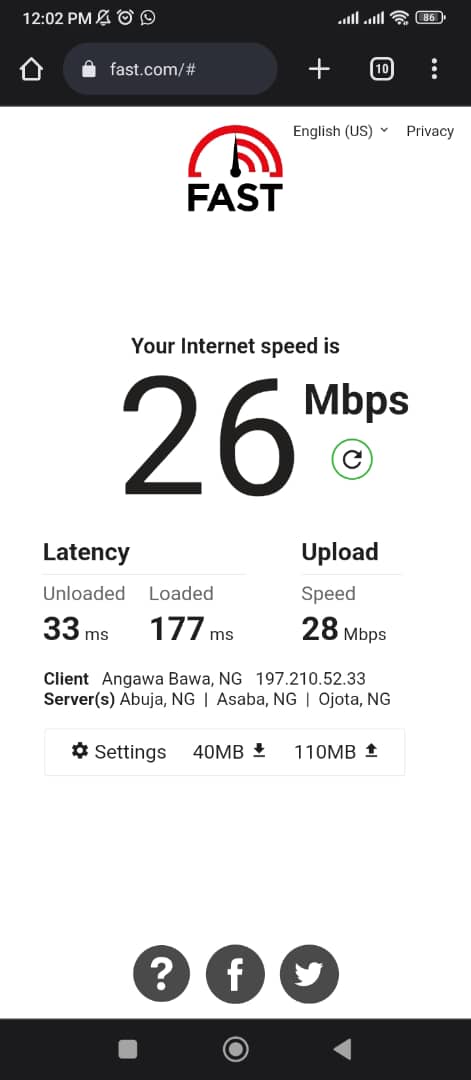

Currently, agency bankers in Vwang use hotspot access via the phone or routers—including MTN 5G router—to power their machines. An internet speed test via Fast.com shows that the average internet speed in Vwang is 26Mbps.

“The network is fair, I rarely have to struggle to get better internet. It was not like this before, we had designated areas where we go to look for network,” a POS operator who identified himself as Don Jay told Premium Times.

Prior to the commencement of phases one and two of the NICTIB project, broadband penetration in Nigeria was 19.8 per cent. However, as of May 2023, the Nigerian Communications Commission disclosed that the penetration now stands at 48.18 per cent.

According to Edidiong Uwemakpan, Head of Global Marketing at Moniepoint, the Nigerian fintech has recorded growth in North Central Nigeria since it started operating in the region—including at Vwang—in 2020.

“We cannot tie this to the broadband because we only expanded there in that period. However, this doesn’t negate the fact that it’ll be difficult to provide optimal services to our users without internet penetration.

”This is because our core product—the Moniepoint PoS terminal—requires the internet to process transactions,” she told Bendada.com.

When this reporter visited Vwang, at least three of every five agency bankers used a Moniepoint terminal. Ms Uwemakpan said that its “android PoS” which is used in the country, including rural communities, runs on 3G, 4G and 5G networks:

“Each PoS terminal can take multiple SIM cards, and the merchant chooses to use the sim with a better connection each time.”

Delays with inter-bank transfers: a threat!

While Internet penetration is driving financial inclusion and development in rural communities, delays with interbank transfers have affected the trust of people in Internet banking.

“I don’t go to the bank or ‘POS people’, I prefer to save what I have with the cooperative society savings or in my house,” Bulus Weng, a commercial farmer and resident of the Vwang community, said.

His discouragement is born from an experience he had transacting with one of the agency bankers. “I needed to send the money to my child in Jos urgently, I gave them [referring to the POS operator] the money, and they claimed that my transfer was made, but it didn’t go through, my child had to borrow money. A week later, they called me to say that the money was reversed,” he narrated. “That day I made up my mind not to go back.”

Mr Weng’s challenge is not unique. Joyce Pius runs a chemist in Vwang, just opposite Vom Christian Hospital—one of the largest healthcare facilities in the community, she does not dispense medicine to patients if a transfer has not been confirmed.

“Just a few minutes before you came in, someone left here, he made a transfer for medicines, but I have not received the alert. I cannot dispense the medicine, you can’t tell if someone is trying to cheat you,” Ms Pius said.

The inter-bank transfer failure goes beyond Vwang, especially during weekends and public holidays.

Last year, the House of Representatives asked the Central Bank of Nigeria (CBN) to address delays arising from instant (inter-bank) electronic funds transfer services in Nigeria with a view to finding a lasting solution to the problem.

Due to poor or inadequate infrastructure, a high influx of transactions affects the performance of inter-bank transfers. “Massive transactions during the weekends hit various platforms, and their volume and processors can’t handle the magnitude of such transactions,” says James Olaibi, Chief Revenue Officer at Nigerian fintech, Airopay.

On its part, the CBN in June 2020 directed banks and other financial institutions to resolve the backlog of all ATM, POS and Web customer refunds within two weeks. The apex bank also issued a revised timeline for dispensing errors and refund complaints.

Following CBN’s demonetisation policy earlier this year that led to a cash crunch across the country, PoS transactions recorded a 40.69 per cent year-on-year increase, according to NIBSS.

Although the official numbers on the growth of financial inclusion in rural communities within Nigeria have yet to be released, a walk around rural communities, including Vwang, shows growth.

“The cash crisis would definitely reaffirm the need for everyone to register on a digital platform and increase financial inclusion in the rural areas,” says Babatunde Obrimah, the chief operating officer of the FinTech Association of Nigeria.

In April, Premium Times reported that the traffic rate on the platforms of organisations under the FinTech Association of Nigeria soared more than fourfold between the start of the cash crunch and the third week of February.

“During the cash scarcity earlier this year, most shops here had to get PoS machines to help with transactions. Also, to avoid inter-bank transfer challenges with traditional banks, many people opted for digital banks like Opay, Palmpay and Moniepoint,” Ms Pius, who uses a Moniepoint PoS terminal, told Bendada.com.

READ ALSO: TECNO and MTN partner to bring lightning-fast internet speeds to Nigerian customers

Since the demonetisation process started—which has now been suspended, Chinese-owned fintech companies Opay and Palmpay have remained the two most downloaded finance apps on Google Play store in Nigeria, alongside other local companies like Kuda and Moniepoint, according to data compiled by Similarweb. These apps rank above those owned by traditional banks.

With NICTIB, telco-owned banks might drive financial inclusion even further

Beyond providing connectivity for communication, Nigerian telco companies are diving into mobile banking.

Last year, the Central Bank of Nigeria (CBN) granted MTN the final approval to operate as Momo Payment Service Bank Limited (Momo PSB), allowing its Nigerian customers to create accounts, pay bills, send and receive money.

According to Lagos-based Enhancing Financial Innovation and Access EfInA, 61% of financially excluded Nigerians have a mobile phone, so they can easily access financial services through USSD or agency bankers.

Aside from MTN, other top telcos, including 9mobile and Glo, have launched mobile banks to bring financial services to their subscribers, especially in rural communities.

This story was produced with support from the Centre for Journalism Innovation and Development (CJID) and funding from the Centre for International Private Enterprise (CIPE)

Support PREMIUM TIMES’ journalism of integrity and credibility

Good journalism costs a lot of money. Yet only good journalism can ensure the possibility of a good society, an accountable democracy, and a transparent government.

For continued free access to the best investigative journalism in the country we ask you to consider making a modest support to this noble endeavour.

By contributing to PREMIUM TIMES, you are helping to sustain a journalism of relevance and ensuring it remains free and available to all.

Donate

TEXT AD: Call Willie – +2348098788999

Until last year, Maureen Pam, a trader, always had to endure trekking to Ganawuri, a district in Plateau’s Riyom area, at the close of Friday market day at Vwang Market in Vom, Jos South.

She was always fear-stricken, caused by her previous experiences with armed robbers on the route, who stole the money she made from her sales that day.

Due to the unavailability of banks in these rural communities, most traders like Ms Pam had to return with the cash from sold goods to their homes, pending when they could access the closest bank, which is located over 60 kilometres from Ganawuri.

“On other weekdays, my daughter would take the money to the bank, but on Fridays, we often had to return with the money since most banks [in Jos-Bukuru metropolis] close early,” she said.

However, she now deposits her money into her bank account via agency bankers (commonly known as POS).

Agency banking allows customers to deposit and withdraw money instead of going to the bank or using ATMs. Currently, there is one agency banking agent for every 80 Nigerians and one bank branch for every 27,000, according to a 2023 report on the Nigerian Financial Services Market.

Although rural communities like Vwang and Ganawuri comprise 53 per cent of Nigeria, the World Bank in 2008 said only 2 per cent of rural households in the country were financially included.

The way out: A National ICT Backbone Project

In a bid to bridge the connectivity gap across the country, the Nigerian government, through its public enterprise Galaxy Backbone Limited signed a commercial contract worth $117 million with Huawei Technologies to commence the first phase of the Nigeria National Information and Communication Technology Infrastructure Backbone (NICTIB) Project.

This phase, completed in August 2018, covered 13 states, including Abuja, Benue, Nassarawa and other states in Southern Nigeria.

According to research by AidData, under the terms of the PBC agreement, the Government of Nigeria was responsible for paying 15 per cent of the cost of the commercial contract with Huawei Technologies Co. Ltd prior to project implementation.

However, Nigeria’s contribution was delayed until December 2006 when Galaxy Backbone Limited made an advance payment of $10 million to Huawei Technologies Co. Ltd. Later, in December 2013, the Federal Ministry of Finance of Nigeria — on behalf of Galaxy Backbone Ltd — completed the payment ($7.65 million) to Huawei to mark the official commencement of the project.

Two years after the completion of the first phase, Galaxy Backbone Limited commenced the second phase worth $328 million—funded via an Export Buyer’s Credit by the Export-Import Bank of China; this phase covers 19 states within Northern Nigeria including Plateau, Kaduna, Bauchi and Gombe, it was also contracted to Huawei Technologies.

In March 2020, Nigeria’s Debt Management Office (DMO) reported that the China Eximbank had disbursed 100 per cent of the original face value of this loan; the final maturity date of this loan being 21 September 2032, after a seven-year grace period.

Meanwhile, as of December 2022, phase two of NICTIB was 98 per cent completed. “At the completion of the project, it will deepen broadband penetration in Nigeria, which is targeted to reach 70% by 2025, up from its current 44.5%,” says Muhammad Abubakar, Managing Director of Galaxy Backbone Limited.

At the time of filing this report, Galaxy Backbone Limited had yet to respond to comments regarding the project’s current status.

According to Retna Daser, a telecom analyst and E.M Application Technologies, the NICTIB has made it easier for telecommunication companies like MTN, GLO and Airtel to rent a portion of the fibre to expand their connectivity into rural communities. “That’s the thing about fibre; multiple companies can route their data through an existing one,” he said.

Currently, agency bankers in Vwang use hotspot access via the phone or routers—including MTN 5G router—to power their machines. An internet speed test via Fast.com shows that the average internet speed in Vwang is 26Mbps.

“The network is fair, I rarely have to struggle to get better internet. It was not like this before, we had designated areas where we go to look for network,” a POS operator who identified himself as Don Jay told Premium Times.

Prior to the commencement of phases one and two of the NICTIB project, broadband penetration in Nigeria was 19.8 per cent. However, as of May 2023, the Nigerian Communications Commission disclosed that the penetration now stands at 48.18 per cent.

According to Edidiong Uwemakpan, Head of Global Marketing at Moniepoint, the Nigerian fintech has recorded growth in North Central Nigeria since it started operating in the region—including at Vwang—in 2020.

“We cannot tie this to the broadband because we only expanded there in that period. However, this doesn’t negate the fact that it’ll be difficult to provide optimal services to our users without internet penetration.

”This is because our core product—the Moniepoint PoS terminal—requires the internet to process transactions,” she told Bendada.com.

When this reporter visited Vwang, at least three of every five agency bankers used a Moniepoint terminal. Ms Uwemakpan said that its “android PoS” which is used in the country, including rural communities, runs on 3G, 4G and 5G networks:

“Each PoS terminal can take multiple SIM cards, and the merchant chooses to use the sim with a better connection each time.”

Delays with inter-bank transfers: a threat!

While Internet penetration is driving financial inclusion and development in rural communities, delays with interbank transfers have affected the trust of people in Internet banking.

“I don’t go to the bank or ‘POS people’, I prefer to save what I have with the cooperative society savings or in my house,” Bulus Weng, a commercial farmer and resident of the Vwang community, said.

His discouragement is born from an experience he had transacting with one of the agency bankers. “I needed to send the money to my child in Jos urgently, I gave them [referring to the POS operator] the money, and they claimed that my transfer was made, but it didn’t go through, my child had to borrow money. A week later, they called me to say that the money was reversed,” he narrated. “That day I made up my mind not to go back.”

Mr Weng’s challenge is not unique. Joyce Pius runs a chemist in Vwang, just opposite Vom Christian Hospital—one of the largest healthcare facilities in the community, she does not dispense medicine to patients if a transfer has not been confirmed.

“Just a few minutes before you came in, someone left here, he made a transfer for medicines, but I have not received the alert. I cannot dispense the medicine, you can’t tell if someone is trying to cheat you,” Ms Pius said.

The inter-bank transfer failure goes beyond Vwang, especially during weekends and public holidays.

Last year, the House of Representatives asked the Central Bank of Nigeria (CBN) to address delays arising from instant (inter-bank) electronic funds transfer services in Nigeria with a view to finding a lasting solution to the problem.

Due to poor or inadequate infrastructure, a high influx of transactions affects the performance of inter-bank transfers. “Massive transactions during the weekends hit various platforms, and their volume and processors can’t handle the magnitude of such transactions,” says James Olaibi, Chief Revenue Officer at Nigerian fintech, Airopay.

On its part, the CBN in June 2020 directed banks and other financial institutions to resolve the backlog of all ATM, POS and Web customer refunds within two weeks. The apex bank also issued a revised timeline for dispensing errors and refund complaints.

Following CBN’s demonetisation policy earlier this year that led to a cash crunch across the country, PoS transactions recorded a 40.69 per cent year-on-year increase, according to NIBSS.

Although the official numbers on the growth of financial inclusion in rural communities within Nigeria have yet to be released, a walk around rural communities, including Vwang, shows growth.

“The cash crisis would definitely reaffirm the need for everyone to register on a digital platform and increase financial inclusion in the rural areas,” says Babatunde Obrimah, the chief operating officer of the FinTech Association of Nigeria.

In April, Premium Times reported that the traffic rate on the platforms of organisations under the FinTech Association of Nigeria soared more than fourfold between the start of the cash crunch and the third week of February.

“During the cash scarcity earlier this year, most shops here had to get PoS machines to help with transactions. Also, to avoid inter-bank transfer challenges with traditional banks, many people opted for digital banks like Opay, Palmpay and Moniepoint,” Ms Pius, who uses a Moniepoint PoS terminal, told Bendada.com.

READ ALSO: TECNO and MTN partner to bring lightning-fast internet speeds to Nigerian customers

Since the demonetisation process started—which has now been suspended, Chinese-owned fintech companies Opay and Palmpay have remained the two most downloaded finance apps on Google Play store in Nigeria, alongside other local companies like Kuda and Moniepoint, according to data compiled by Similarweb. These apps rank above those owned by traditional banks.

With NICTIB, telco-owned banks might drive financial inclusion even further

Beyond providing connectivity for communication, Nigerian telco companies are diving into mobile banking.

Last year, the Central Bank of Nigeria (CBN) granted MTN the final approval to operate as Momo Payment Service Bank Limited (Momo PSB), allowing its Nigerian customers to create accounts, pay bills, send and receive money.

According to Lagos-based Enhancing Financial Innovation and Access EfInA, 61% of financially excluded Nigerians have a mobile phone, so they can easily access financial services through USSD or agency bankers.

Aside from MTN, other top telcos, including 9mobile and Glo, have launched mobile banks to bring financial services to their subscribers, especially in rural communities.

This story was produced with support from the Centre for Journalism Innovation and Development (CJID) and funding from the Centre for International Private Enterprise (CIPE)

Support PREMIUM TIMES’ journalism of integrity and credibility

Good journalism costs a lot of money. Yet only good journalism can ensure the possibility of a good society, an accountable democracy, and a transparent government.

For continued free access to the best investigative journalism in the country we ask you to consider making a modest support to this noble endeavour.

By contributing to PREMIUM TIMES, you are helping to sustain a journalism of relevance and ensuring it remains free and available to all.

Donate

TEXT AD: Call Willie – +2348098788999

Denial of responsibility! Techno Blender is an automatic aggregator of the all world’s media. In each content, the hyperlink to the primary source is specified. All trademarks belong to their rightful owners, all materials to their authors. If you are the owner of the content and do not want us to publish your materials, please contact us by email – [email protected]. The content will be deleted within 24 hours.